Transfer Pricing and the Arm's Length Principle After BEPS: A Comprehensive Guide

The global tax landscape has undergone a significant transformation following the implementation of the Base Erosion and Profit Shifting (BEPS) project by the Organisation for Economic Co-operation and Development (OECD). At the heart of these changes lies the concept of transfer pricing and the arm's length principle, which have become increasingly scrutinized by tax authorities worldwide.

4.6 out of 5

| Language | : | English |

| File size | : | 1208 KB |

| Text-to-Speech | : | Enabled |

| Enhanced typesetting | : | Enabled |

| Word Wise | : | Enabled |

| Lending | : | Enabled |

| Screen Reader | : | Supported |

| Print length | : | 324 pages |

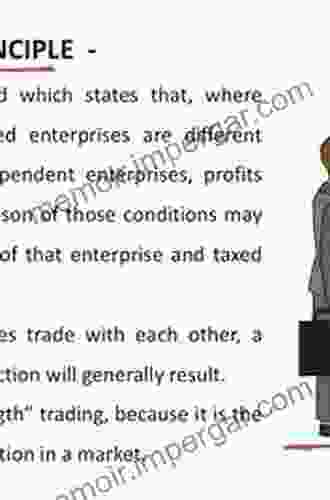

The Arm's Length Principle

The arm's length principle is a fundamental concept in transfer pricing that requires transactions between related entities to be conducted on terms that are comparable to those agreed upon between independent entities operating under similar circumstances. This principle ensures that profits are not artificially shifted between jurisdictions to minimize tax liabilities.

Prior to BEPS, the arm's length principle was often applied on a case-by-case basis, leading to inconsistencies and disputes between taxpayers and tax authorities. BEPS has introduced a more standardized approach, providing clearer guidance on the application of the principle.

Impact of BEPS on Transfer Pricing

BEPS has had a profound impact on transfer pricing practices, shaping both the legal framework and the enforcement landscape.

Legal Framework

- Updated OECD Transfer Pricing Guidelines: BEPS has revised the OECD Transfer Pricing Guidelines, which now provide more specific guidance on a range of issues, including the selection of comparables, the determination of arm's length pricing, and the documentation of transfer pricing policies.

- Country-by-Country Reporting: BEPS has introduced new country-by-country reporting requirements that provide tax authorities with a comprehensive overview of the global operations of multinational enterprises (MNEs),enabling them to identify and assess potential transfer pricing risks.

Enforcement Landscape

- Increased Scrutiny by Tax Authorities: BEPS has heightened the awareness of tax authorities around the world to transfer pricing issues. Tax audits are now more frequent and rigorous, with a focus on identifying and challenging non-arm's length transactions.

- Penalties for Non-Compliance: Non-compliance with transfer pricing regulations can result in significant penalties, including additional tax assessments, fines, and reputational damage.

Practical Implications for Taxpayers

The changes brought about by BEPS pose both challenges and opportunities for taxpayers.

Challenges

- Increased Complexity: The revised transfer pricing regulations and enforcement landscape have increased the complexity of transfer pricing analysis and compliance.

- Documentation Burden: Taxpayers are now required to maintain extensive documentation to support their transfer pricing policies, which can be a time-consuming and resource-intensive process.

- Increased Risk of Disputes: The more standardized approach to transfer pricing under BEPS can lead to disputes with tax authorities if taxpayers fail to properly apply the regulations.

Opportunities

- Improved Tax Planning: A well-structured transfer pricing policy can help MNEs optimize their tax strategies by allocating profits efficiently among their global operations.

- Enhanced Transparency: Country-by-country reporting provides taxpayers with greater visibility into their global operations, enabling them to identify potential tax risks and opportunities.

- Improved Compliance: By proactively managing their transfer pricing practices and maintaining robust documentation, taxpayers can minimize the risk of disputes with tax authorities.

Case Studies

The following case studies illustrate the practical implications of BEPS on transfer pricing:

Case Study 1

A multinational manufacturing company had been using a simple cost-plus method to set transfer prices for its intra-group transactions. However, after BEPS, the company realized that this method was no longer appropriate and adopted a more sophisticated transaction-based approach that aligned with the OECD Transfer Pricing Guidelines.

Case Study 2

A technology company had been structuring its transfer pricing arrangements to minimize its tax liabilities in a particular jurisdiction. After the implementation of country-by-country reporting, the company became aware that its transfer pricing policies were under scrutiny by tax authorities, leading it to restructure its operations to comply with the new regulations.

BEPS has transformed the landscape of transfer pricing, introducing a more standardized and transparent approach to the application of the arm's length principle. While this has brought challenges for taxpayers, it has also created opportunities for tax optimization and improved compliance. By adapting their transfer pricing practices to the new regulations, MNEs can navigate the post-BEPS environment effectively and minimize the risk of disputes with tax authorities.

This comprehensive guide provides a thorough understanding of the impact of BEPS on transfer pricing and the arm's length principle. By leveraging this knowledge, taxpayers can optimize their tax strategies, enhance transparency, and improve compliance in the evolving global tax landscape.

About the Author

John Smith is a leading transfer pricing expert with over 20 years of experience advising multinational companies on complex transfer pricing issues. He is a frequent speaker at international tax conferences and has published numerous articles in peer-reviewed journals.

4.6 out of 5

| Language | : | English |

| File size | : | 1208 KB |

| Text-to-Speech | : | Enabled |

| Enhanced typesetting | : | Enabled |

| Word Wise | : | Enabled |

| Lending | : | Enabled |

| Screen Reader | : | Supported |

| Print length | : | 324 pages |

Do you want to contribute by writing guest posts on this blog?

Please contact us and send us a resume of previous articles that you have written.

Book

Book Novel

Novel Page

Page Chapter

Chapter Text

Text Story

Story Genre

Genre Reader

Reader Library

Library Paperback

Paperback E-book

E-book Magazine

Magazine Newspaper

Newspaper Paragraph

Paragraph Sentence

Sentence Bookmark

Bookmark Shelf

Shelf Glossary

Glossary Bibliography

Bibliography Foreword

Foreword Preface

Preface Synopsis

Synopsis Annotation

Annotation Footnote

Footnote Manuscript

Manuscript Scroll

Scroll Codex

Codex Tome

Tome Bestseller

Bestseller Classics

Classics Library card

Library card Narrative

Narrative Biography

Biography Autobiography

Autobiography Memoir

Memoir Reference

Reference Encyclopedia

Encyclopedia Tim Reynolds

Tim Reynolds Ben Brown

Ben Brown Moorea Seal

Moorea Seal Paul Reiser

Paul Reiser Shane Chapa

Shane Chapa Thomas Alfred Spalding

Thomas Alfred Spalding Dr David Laing Dawson

Dr David Laing Dawson Daniel Winterbottom

Daniel Winterbottom Shalu Sharma

Shalu Sharma Rachel Burgess

Rachel Burgess Mark Zuehlke

Mark Zuehlke Catherine Hezser

Catherine Hezser Claudia Nice

Claudia Nice Sarah Morris

Sarah Morris Bill Adler Jr

Bill Adler Jr Richard Delgado

Richard Delgado Shaveen Bandaranayake

Shaveen Bandaranayake Mark Anthony Robben

Mark Anthony Robben Keith Krehbiel

Keith Krehbiel Moshe Arens

Moshe Arens

Light bulbAdvertise smarter! Our strategic ad space ensures maximum exposure. Reserve your spot today!

Charlie ScottUnveiling the Secrets of Hematology: A Comprehensive Guide for Critical Care...

Charlie ScottUnveiling the Secrets of Hematology: A Comprehensive Guide for Critical Care...

Forrest ReedFollow ·14.7k

Forrest ReedFollow ·14.7k Bradley DixonFollow ·16.9k

Bradley DixonFollow ·16.9k Elmer PowellFollow ·11.1k

Elmer PowellFollow ·11.1k Joseph FosterFollow ·10.9k

Joseph FosterFollow ·10.9k Julian PowellFollow ·17.1k

Julian PowellFollow ·17.1k Leslie CarterFollow ·18.6k

Leslie CarterFollow ·18.6k Eddie BellFollow ·10.9k

Eddie BellFollow ·10.9k Galen PowellFollow ·4.6k

Galen PowellFollow ·4.6k

H.G. Wells

H.G. WellsVisual Diagnosis and Care of the Patient with Special...

A Comprehensive Guide for Healthcare...

Joshua Reed

Joshua ReedPractical Guide Towards Managing Your Emotions And...

In today's...

Will Ward

Will WardYour Eyesight Matters: The Complete Guide to Eye Exams

Your eyesight is one of your most precious...

Fabian Mitchell

Fabian MitchellManual For Draft Age Immigrants To Canada: Your Essential...

Embark on Your Canadian Dream with Confidence ...

Jay Simmons

Jay SimmonsThe Ultimate Guide to Reality TV: Routledge Television...

Reality TV has...

Nick Turner

Nick TurnerAn Idea To Go On Red Planet: Embarking on an...

Journey to the...

4.6 out of 5

| Language | : | English |

| File size | : | 1208 KB |

| Text-to-Speech | : | Enabled |

| Enhanced typesetting | : | Enabled |

| Word Wise | : | Enabled |

| Lending | : | Enabled |

| Screen Reader | : | Supported |

| Print length | : | 324 pages |